I wish I knew where I am going to die, and then I'd never go there

Things you should know before reading and remember after reading

I already own share

Human beings are rationalizing than rational . may be I am trying to justify my current ownership

Man with a hammer

I have been reading up about value investing and stock markets for some time now. So maybe I am a man with a hammer for whom everything looks like a nail.

Novice

I don’t have any stock market investing experience. Buying share is an exercise in arrogance. You say that your judgments is superior than others . When I combine this with that of my lack of experience it can produce truly horrible .

Authority influence

I quote several respected investors. While my objective is vicarious learning - beware it might influence you.

JK Bank Comments

Strengths/Moats

1. Niche geographic presence. Enjoys virtual monopoly in J&K . Which ensures stable depositor base. “consumer based, small business type huge deposit base”

2. Unique characteristics of J&K ensures low cost of deposits without significant float from cash management, settlement income etc

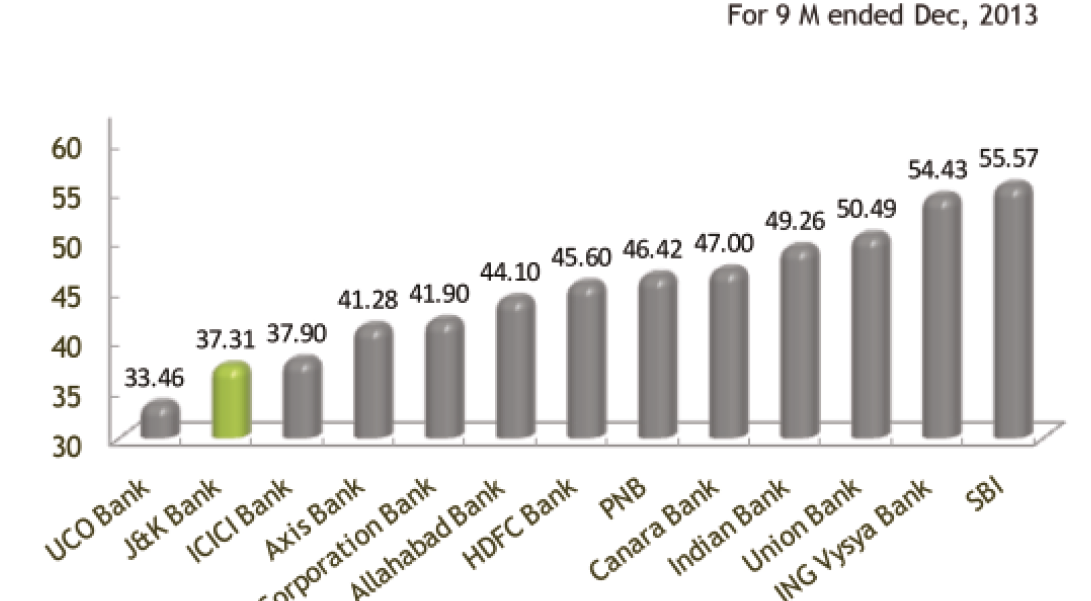

Cost to income is basically the amount of operational expense per rupee of income. Hence lower the better. Management hope to maintain the trend even after the wage hike (already reflecting in financials and new CSR provision) To really appreciate the strength of this See below the comparable cost to income ratio

4. Management - I think not really able to manage analysts

6. Valuation

I already own share

Human beings are rationalizing than rational . may be I am trying to justify my current ownership

Man with a hammer

I have been reading up about value investing and stock markets for some time now. So maybe I am a man with a hammer for whom everything looks like a nail.

Novice

I don’t have any stock market investing experience. Buying share is an exercise in arrogance. You say that your judgments is superior than others . When I combine this with that of my lack of experience it can produce truly horrible .

Authority influence

I quote several respected investors. While my objective is vicarious learning - beware it might influence you.

JK Bank Comments

Strengths/Moats

1. Niche geographic presence. Enjoys virtual monopoly in J&K . Which ensures stable depositor base. “consumer based, small business type huge deposit base”

2. Unique characteristics of J&K ensures low cost of deposits without significant float from cash management, settlement income etc

- Government business completely done by J&K Bank >> Large float

- Muslim dominated customer population – aversion to interest

Cost to income is basically the amount of operational expense per rupee of income. Hence lower the better. Management hope to maintain the trend even after the wage hike (already reflecting in financials and new CSR provision) To really appreciate the strength of this See below the comparable cost to income ratio

4. Management - I think not really able to manage analysts

- not really getting the questions, really not very polished, casual way of talking ( CEO calls the analyst my friend etc !) but seems to be very hands on operation focused.

- Management has grown within the bank

- Focused on shareholder ( or the need to please government – largest shareholder ?

JK Bank to sacrifice profit to maintain dividend - But going by the NPA numbers reported and all through so called consortium lending ( loosing :) ) arrangement looks like they have got in to bad company. And the share price now adjusted to this - “A man is known by the company he keeps”.

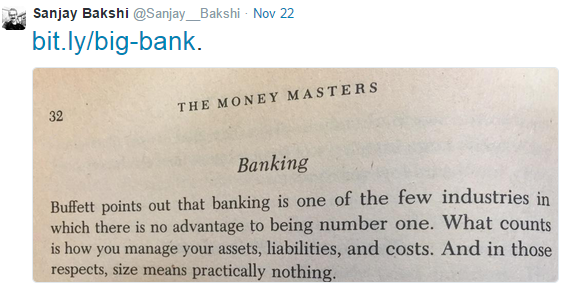

- To quote Buffett : “ mistakes have been the rule rather than the exception at many major banks. Most have resulted from a managerial failing that we described last year when discussing the "institutional imperative:" the tendency of executives to mindlessly imitate the behavior of their peers, no matter how foolish it may be to do so. In their lending, many bankers played follow-the-leader with lemming-like zeal; now they are experiencing a lemming-like fate

- He is a good spokesman apart from the credentials as a value investor ( if you doubt see this youtube link - watch from 1:43:50).

- He uses check lists extensively and never invests if it is at least a 2x

- You can buy now 20% discount to what he paid ( Anchoring bias !)

- Just to balance this please see the comment by Sanjay.

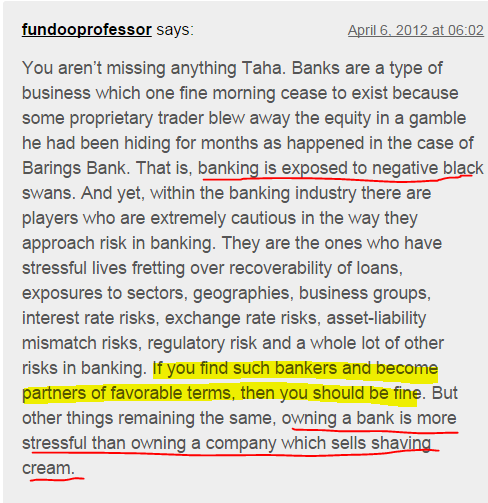

- Also keep in mind that Prof is not a fan of banking stocks :

Anyways to quote Buffett “Public opinion poll is not substitute for thought….Derive no comfort from intelligent people, vocal people or majority of people …..if we are in a situation that we can understand, facts are ascertainable and clear >> we are progressing in a conservative way” )

Please see below the P&L in INR crores

- At present levels ( 4600 crores; 95 a share) the bank is available at

- a. Less than Four times after tax and around 2.7 times pre-tax earnings based on Fy 2014 earning.

- b. Less than Six times pre-tax earnings and around 9 times after tax earnings based on a current run rate FY 2015 earning. This assumes a bad debt provision of 670 croes for the financial year. Which means that assuming no growth and provision of 500 crore for bad debt every year- investment will be cash flow neutral every year.

- Bank had excellent return on equity in the past and good compounder = logically eligible for higher valuation

- If you want to see more optimistic valuation scenario you can hear how Mohnish is looking at this investment.

- JK bank hold 102.2 million shares in Metlife which the CEO expects to fetch at least RS 80 a share. Even if we discount the valuation optimism by 60% – it will completely offset the bad debts booked in FY 2015. Earlier they did a partial stake sale to Metlife – now it would be much easier due to FDI investment limit enhancement.

“The first chance you have, to avoid a loss from a foolish loan is by refusing to make it; there is no second chance – Munger”

There is no doubt they are in a deep mess as of now. Floods, High level corporate debt default and allegations about book fudging. So they already missed their first chance very terribly.

Now only thing that is worth considering is “Bad Debt Related Issues are One Foot hurdles they could step over ? “We don't leap seven-foot fences. Instead, we look for one-foot fences with big rewards on the other side. So we've succeeded by making the world easy for ourselves, not by solving hard problems- Munger”

I think the odds are in favor of management in climbing this NPA mess

- They have handled this monster in the past – FY 97 had 6% NPA

- Management commitment that corporate lending will be restricted to Govt of India and good corporates

- I am not able to see any fundamental changes in the risk management and culture of the bank - Except misjudgment and bad company with other inefficient PSU banks through consortium loosing arrangement.

- Given the best cost to income ratio – management has tremendous room to manage this mess

- All competitive advantages remain unaffected – management energy can be focused on arresting NPA.

posted by Mithun at

8:02 PM

|

3 comments

![]()